Table of Contents

Why PBM Reform Is Dominating Healthcare Policy in 2026

The healthcare landscape is shifting. For years, the complexity of drug pricing has remained a persistent challenge for American families and businesses.

In 2026, we are seeing a fundamental move toward transparency and accountability.

The CAA of 2026: Turning Bipartisan Pressure into Federal Law

The passage of the Consolidated Appropriations Act of 2026 (CAA 2026) represents a landmark shift in federal oversight.

This legislation directly addresses the structural opaque nature of Pharmacy Benefit Managers.

By mandating 100% rebate pass through and “delinking” PBM compensation from drug list prices, the law moves the industry away from misaligned incentives.

It effectively reclassifies PBMs as “covered service providers” under federal standards, ensuring that savings actually reach the plans and the patients.

The CAA 2026 authorizes civil penalties of up to $10,000 per day for PBMs that fail to comply with new reporting and compensation disclosure requirements.

Drug Affordability as a Top Tier Issue in the 2026 Election Cycle

As we approach the midterm elections, healthcare costs have moved to the center of the national conversation.

Access to affordable medicine is no longer a secondary concern; it is a primary economic driver for voters. Federal initiatives, including the expansion of the Medicare Drug Price Negotiation Program, have set a new precedent for how the government interacts with the pharmaceutical supply chain to lower out of pocket costs.

According to the KFF Health Tracking Poll, more than 4 in 10 voters report that the cost of healthcare will have a major impact on their vote in the 2026 midterms.

Self-Insured Plans Utilizing New Fiduciary Powers

The Department of Labor is providing plan sponsors with the tools they need to manage their healthcare spend.

New proposed rules under ERISA Section 408(b)(2) empower fiduciaries of self-insured plans to look inside the “black box” of PBM pricing.

With enhanced audit rights and mandatory disclosures regarding spread pricing and manufacturer fees, employers can now verify if their PBM arrangements are truly reasonable and necessary.

Federal Trade Commission (FTC) research into PBM practices revealed that specialty generic drugs were often marked up by hundreds or thousands of percentage points when dispensed through PBM-affiliated pharmacies.

What PBMs Actually Do

Understanding the healthcare supply chain requires a clear look at the roles played by intermediaries.

Pharmacy Benefit Managers (PBMs) operate at the intersection of drug manufacturers, insurers, and pharmacies, exerting significant influence over which medications are available and at what cost.

Role: Negotiators, Formulary Gatekeepers, and Network Managers

PBMs perform several core functions designed to manage drug spend.

- As negotiators, they leverage the collective volume of their members to secure rebates from manufacturers.

- As formulary gatekeepers, they decide which drugs are “preferred” on a plan’s list, often determining a patient’s out-of-pocket cost through tiered co-pays.

- Finally, as network managers, they establish the group of pharmacies where patients can fill prescriptions, setting the reimbursement rates that pharmacies receive for their services.

According to 2024 Federal Trade Commission (FTC) research, the three largest PBMs processed approximately 80% of the 6.6 billion prescriptions dispensed in the United States.

The Conflict: Why the "Big Three" Face Unprecedented Antitrust Scrutiny

The concentration of market power among CVS Caremark, Express Scripts, and OptumRx has led to increased federal oversight.

The primary concern is vertical integration, where a single corporate entity owns the insurer, the PBM, and the pharmacy.

This structure can create misaligned incentives, such as “steering” patients toward PBM-owned specialty pharmacies or favoring high-list-price drugs that offer larger rebates over lower-cost alternatives.

In 2026, the FTC and Department of Justice (DOJ) have intensified legal actions to address these “unfair methods of competition” that may artificially inflate costs.

A landmark 2026 FTC settlement with a major PBM is projected to deliver up to $7 billion in patient savings on out-of-pocket pharmaceutical costs over the next 10 years by altering formulary practices.

Definition Update: Formalizing "PBM Affiliates" and GPOs

The Consolidated Appropriations Act of 2026 (CAA 2026) closed a significant loophole by expanding the legal definition of a PBM.

The law now formally includes “PBM Affiliates,” which covers rebate aggregators and Group Purchasing Organizations (GPOs).

Historically, PBMs could move revenue to these offshore or secondary entities to avoid “pass-through” requirements.

Under the new federal standard, any entity that acts as a price negotiator or group purchaser on behalf of a plan (regardless of its corporate label) is subject to the same transparency and fiduciary mandates.

The CAA 2026 requires PBMs to remit 100% of rebates to plans within 90 days of each quarter, with a tightened 45-day window for funds moving from rebate aggregators or GPOs to the PBM.

The 2026 Policy Landscape: Federal and State Momentum

The intersection of federal law and aggressive state enforcement has created a new operational reality for the American healthcare system.

For plan sponsors and healthcare providers, 2026 is the year where “transparency” moved from a buzzword to a series of strict legal mandates with significant financial consequences.

Federal Law (CAA 2026): The $1.2T Regulatory Shift

The Consolidated Appropriations Act of 2026 (CAA 2026) is the most significant healthcare reform since the Affordable Care Act.

This legislation fundamentally restructures the PBM business model by mandating rebate pass-throughs and the delinking of service fees from drug list prices in Medicare Part D.

By forcing PBMs to accept only “flat, bona fide service fees,” the law eliminates the incentive for PBMs to favor high-priced medications that offer larger rebates.

This federal standard is now migrating into the commercial sector as plan fiduciaries demand the same protections for private employer-sponsored insurance.

The CAA 2026 establishes a federal mandate that 100% of manufacturer rebates must be passed through to the plan sponsor, removing the “rebate retention” model that previously allowed PBMs to keep a portion of these discounts.

The FTC Settlement: Express Scripts and Net-Price Benchmarking

In February 2026, the Federal Trade Commission (FTC) finalized a landmark consent order with Express Scripts.

This settlement serves as a blueprint for the industry’s new “Standard Offering.” Under the order, the PBM must offer plan designs that base patient cost-sharing on the net price of a drug (the price after rebates) rather than the inflated list price.

This shift directly addresses the “rebate trap” where patients were paying higher co-insurance for medications that were technically cheaper for the PBM to acquire.

The FTC projects that the Express Scripts settlement alone will deliver up to $7 billion in patient savings on out-of-pocket pharmaceutical costs over the next decade.

The DOL Transparency Rule: Mandated Disclosures for Self-Insured Plans

Starting July 1, 2026, the Department of Labor (DOL) will enforce new transparency requirements under ERISA Section 408(b)(2).

These rules require PBMs to provide “covered service provider” disclosures to self-insured plan fiduciaries.

These disclosures must include detailed, drug-level reporting on both direct and indirect compensation, including spread pricing and claw-backs.

This rule effectively empowers HR departments and benefits committees to audit their PBMs with the same rigor used for pension fund managers.

Failure to provide these mandatory disclosures renders the PBM contract “unreasonable” under ERISA, exposing PBMs to Department of Labor enforcement and civil litigation from plan participants.

State Progress: California’s SB 41 and Washington’s E2SSB 5213

While federal law sets the floor, states like California and Washington are setting a higher ceiling.

Effective January 1, 2026, California’s SB 41 and Washington’s E2SSB 5213 officially banned spread pricing—the practice where a PBM charges a plan more than it pays the pharmacy.

These laws also include “any willing pharmacy” provisions and “anti-steering” protections, preventing PBMs from forcing patients to use PBM-owned mail-order pharmacies.

Under California’s SB 41, PBMs must now obtain licensure from the Department of Managed Health Care (DMHC) and are subject to regular financial examinations to verify they are not retaining hidden spreads.

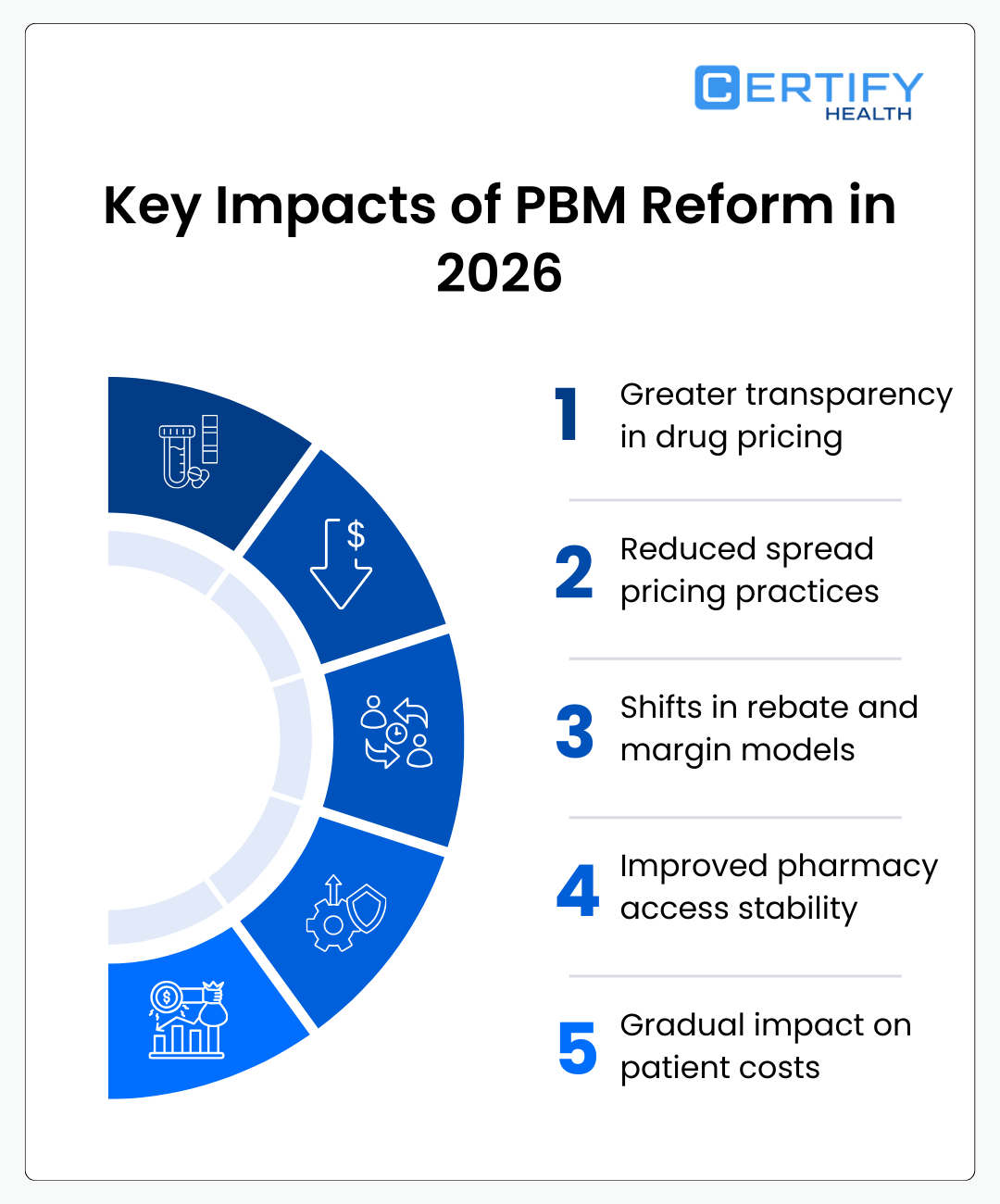

Key PBM Reforms Taking Shape in 2026

The current regulatory environment is focused on eliminating the structural opacity that has historically characterized the pharmacy benefit manager industry.

By codifying transparency and realigning financial incentives, the federal government is moving toward a market where competition is based on value and clinical outcomes rather than arbitrage.

1. Transparency & "Standardized Definitions"

A significant challenge in healthcare oversight has been the lack of uniform terminology. Under the CAA 2026, federal regulators have established consistent, mandatory definitions for drug classifications such as “Brand,” “Generic,” and “Specialty.”

Historically, PBMs could manipulate these categories—often labeling certain generics as “specialty”—to apply higher margin structures.

The new law mandates semiannual drug-level reporting to plan fiduciaries, providing granular data on net spending and any retained manufacturer revenue.

The CAA 2026 authorizes civil penalties of up to $10,000 per day for PBMs or plans that fail to provide the required transparency reports or drug-level data.

2. The Ban on Spread Pricing & "Delinking"

Federal policy is aggressively shifting PBM compensation from a percentage-based model to Bona Fide Service Fees.

This process, known as “delinking,” ensures that a PBM’s profit is not tied to the list price of a medication or the volume of rebates generated. In the Medicare Part D market, this is now a legal requirement, effectively setting the “finish line” for reform.

For the commercial market, “Standard Offerings” serve as the starting line, allowing self-insured employers to demand flat-fee models that remove the incentive for PBMs to prefer expensive drugs over lower-cost alternatives.

According to the Congressional Budget Office (CBO), delinking PBM compensation from drug list prices in federal programs is projected to reduce the federal deficit by $11 billion over 10 years by lowering overall drug spend.

3. 100% Rebate Pass-Through

The era of rebate retention is ending. Federal law now requires PBMs to remit 100% of all manufacturer revenue (including rebates, volume discounts, and administrative fees) directly to the plan sponsor.

Furthermore, the FTC has targeted “rebate aggregators,” often offshore entities like Ascent Health Services, requiring them to reshore operations to the United States.

This ensures that these entities fall under the jurisdiction of U.S. auditors and federal investigators, preventing PBMs from hiding revenue in international subsidiaries.

The CAA 2026 requires that 100% of manufacturer rebates be remitted to plan sponsors within 90 days of the end of each quarter, with a tighter 45-day window for funds processed through rebate aggregators.

4. "Essential Retail Pharmacy" Protections

To protect the healthcare infrastructure in rural and underserved communities, the 2026 reforms introduce the “Essential Retail Pharmacy” designation.

This legal status applies to independent pharmacies that are not affiliated with a PBM and serve as the sole access point within a specific radius (e.g., 10 miles in rural areas).

The law prohibits PBMs from engaging in “reimbursement discrimination,” meaning they cannot pay these essential independent pharmacies less than they pay their own PBM-affiliated retail or mail-order stores.

Recent data from the University of Southern California (USC) Schaeffer Center shows that nearly one-third of independent pharmacies in the U.S. closed between 2010 and 2021, a trend the new “Essential” designation aims to reverse.

How PBM Reform Impacts Drug Costs

The structural changes enacted in 2026 are designed to move the pharmacy benefit model from a high-list-price system to a net-price reality. This shift is already manifesting in reduced out-of-pocket costs for the most common chronic condition medications.

Short-Term: Immediate Relief on "Negotiated Drugs"

2026 marks the first year that Maximum Fair Prices (MFP) take effect for the initial ten drugs selected under the Inflation Reduction Act’s Medicare Drug Price Negotiation Program. Medications such as Eliquis, Januvia, and Jardiance now have federally negotiated price caps.

Because PBMs are prohibited from applying traditional “spread” or administrative markups on these specific products, the savings flow directly to the program and the patient.

According to the Centers for Medicare & Medicaid Services (CMS), the negotiated prices for these initial ten drugs represent an average reduction of 38% to 79% off the 2023 list prices.

Point-of-Sale (POS) Rebates: Savings at the Counter

A critical shift in 2026 is the transition to Point-of-Sale (POS) rebates. Historically, PBMs collected rebates months after a patient purchased a drug, often keeping a portion or returning it to the employer as a “back-end” check.

New federal guidance under the CAA 2026 encourages plans to apply these discounts at the pharmacy counter. This ensures that a patient’s coinsurance is calculated based on the lower, post-rebate cost rather than the artificial list price.

The Department of Health and Human Services (HHS) estimates that mandatory POS rebate pass-throughs will save seniors an average of $125 per year in direct out-of-pocket costs.

What It Means for Patient Access to Medications

Policy reform is all about the reliability of the pharmacy experience. The 2026 landscape is prioritizing clinical stability over financial arbitrage.

The "TrumpRx" Integration: Direct-to-Consumer Models

The 2026 policy environment has paved the way for “TrumpRx” style integrations, where direct-to-consumer (DTC) pharmacy models—like those offering transparent “cost-plus” pricing—are now being formally integrated into traditional insurance networks.

By removing the PBM as the exclusive intermediary, these models allow patients to use their insurance benefits at transparent providers who do not participate in complex rebate schemes.

A 2026 report from the Congressional Research Service (CRS) indicates that incorporating “cost-plus” pharmacy options into federal employee health plans could reduce administrative overhead by 15% per prescription.

Formulary Stability and Narrower Networks

Reform is putting an end to “rebate chasing,” where PBMs would switch a patient’s preferred medication mid-year simply because a different manufacturer offered a higher rebate.

The CAA 2026 limits mid-year formulary changes to clinical necessity only. However, a potential risk remains: as PBMs lose rebate revenue, they may seek to consolidate “preferred” networks even further to extract higher volume discounts from specific retail chains.

Under new 2026 Medicare Part D rules, plans must provide at least 60 days of notice before making any formulary changes, up from the previous 30-day standard.

Winners and Losers of PBM Reform

The redistribution of value in the 2026 healthcare market is creating clear distinctions between legacy models and transparent innovators.

Winners: Independent Pharmacies and Plan Fiduciaries

- Independent Pharmacies: Benefiting from “Essential Retail Pharmacy” protections and the ban on “DIR fees” (Direct and Indirect Remuneration), these small businesses are seeing stabilized reimbursement rates.

- Plan Fiduciaries: Employers and union trust funds now have the legal standing to audit their PBMs without the “trade secret” barriers that previously hid pricing data.

- Seniors: The elimination of the “coverage gap” (or donut hole) combined with a $2,000 annual out-of-pocket cap provides unprecedented financial security.

Losers: Spread-Pricing and Offshore Aggregators

- Traditional PBMs: Entities reliant on “the spread” (the difference between what they charge the plan and pay the pharmacy) are seeing their primary profit engine dismantled.

- Offshore Aggregators: Entities like Ascent and Zinc face “reshoring” mandates that subject their books to Department of Labor and FTC oversight.

Action Step

The regulatory window for 2026 compliance is now open.

To ensure your organization is capturing the 100% rebate pass-through mandates and avoiding “spread” liabilities, you must update your service provider agreements.

Action Steps for Employers and Health Plans

The window for voluntary compliance has closed.

In 2026, plan sponsors must transition from passive oversight to active fiduciary management to meet new federal benchmarks.

Audit Immediately: Verifying 2025-2026 Rebate Compliance

Under the CAA 2026, the “Right to Audit” is no longer a negotiated contract term; it is a federally mandated annual requirement.

Employers must verify that 100% of manufacturer revenue (including credits from offshore rebate aggregators) has been correctly attributed to the plan.

This audit should focus on identifying hidden “administrative fees” that may have been used to bypass rebate pass-through requirements during the 2025 transition period.

- The Department of Labor (DOL) estimates that proactive fiduciary auditing can recover an average of $3 to $5 per member per month (PMPM) in previously undisclosed PBM retained revenue.

Contract Leveraging: The $10,000-Per-Day Penalty

As negotiations for the 2027 plan year begin, fiduciaries should utilize the federal enforcement framework as leverage.

The CAA 2026 imposes significant financial penalties on PBMs that fail to provide drug-level transparency or compensation disclosures.

Using these statutory requirements as a baseline ensures that your next contract is built on a “transparent-only” framework, eliminating the need to negotiate for data that is now legally yours.

Federal law now authorizes civil penalties of up to $10,000 per day against service providers who fail to comply with the transparency and disclosure mandates of ERISA Section 408(b)(2).

Fiduciary Responsibility: "Ignoring the Data" as a Legal Liability

In 2026, plan sponsors can no longer claim ignorance of PBM pricing structures.

The Department of Labor’s 2026 Compliance Guidance clarifies that failing to review mandated transparency reports constitutes a breach of fiduciary duty.

If a plan pays more for a drug through a PBM than the “Maximum Fair Price” or a “Standard Offering” price without justification, the plan trustees may be held personally liable for the overpayment.

A 2026 GAO report found that over 60% of ERISA-related litigation now involves claims of “excessive fees” related to pharmacy benefit management and administrative costs.

Common Misconceptions About PBM Reform

As the industry adjusts to the new regulatory reality, several myths persist that can lead to non-compliance and financial loss for plan sponsors.

"The law doesn't matter until 2028"

While some long-term structural changes have multi-year phase-in periods, the core transparency and “delinking” requirements for Medicare and the disclosure mandates for private plans are active as of January 1, 2026.

Between the FTC’s February 2026 consent orders and the DOL’s July 1 enforcement deadline, 2026 is the primary year of implementation.

Waiting until 2028 to modernize your pharmacy benefit strategy ignores current legal requirements and immediate savings opportunities.

"Rebates will vanish"

Rebates are not disappearing; they are being rerouted. The “delinking” movement does not eliminate manufacturer discounts; it simply mandates that those discounts must benefit the payer and the patient rather than the PBM’s bottom line.

The volume of rebates remains high, but the PBM’s ability to retain them as “spread” or “administrative fees” has been legally restricted.

Data from the Centers for Medicare & Medicaid Services (CMS) shows that despite delinking efforts, total manufacturer rebates in the U.S. market are projected to reach $250 billion in 2026, with nearly 98% now being passed through to plan sponsors.

Conclusion: The New "Standard Offering"

The era of the “Black Box” has officially ended.

In 2026, the “Standard Offering” for pharmacy benefits is defined by transparency first.

The shift from percentage-based compensation to flat, bona fide service fees has realigned the industry, ensuring that PBMs are rewarded for managing health outcomes rather than maximizing drug list prices.

2026 stands as the year the pharmaceutical supply chain was finally illuminated, providing American employers and families with the clarity they have long deserved.

CERTIFY Health

Stay ahead of the 2026 transparency mandates.

CERTIFY Health’s compliance dashboard provides real-time auditing and automated reporting to ensure your PBM is meeting every federal requirement. Book a demo to Learn more.